CRE Owners and Operators: Leverage Public REIT Strategies to Capitalize Opportunities

- News & Insights

- Public REIT Strategies, Private CRE Owners & Operators, Capitalize Opportunities

- September 20, 2023

What Private CRE Owners & Operators Can Learn From Their Public REIT Peers

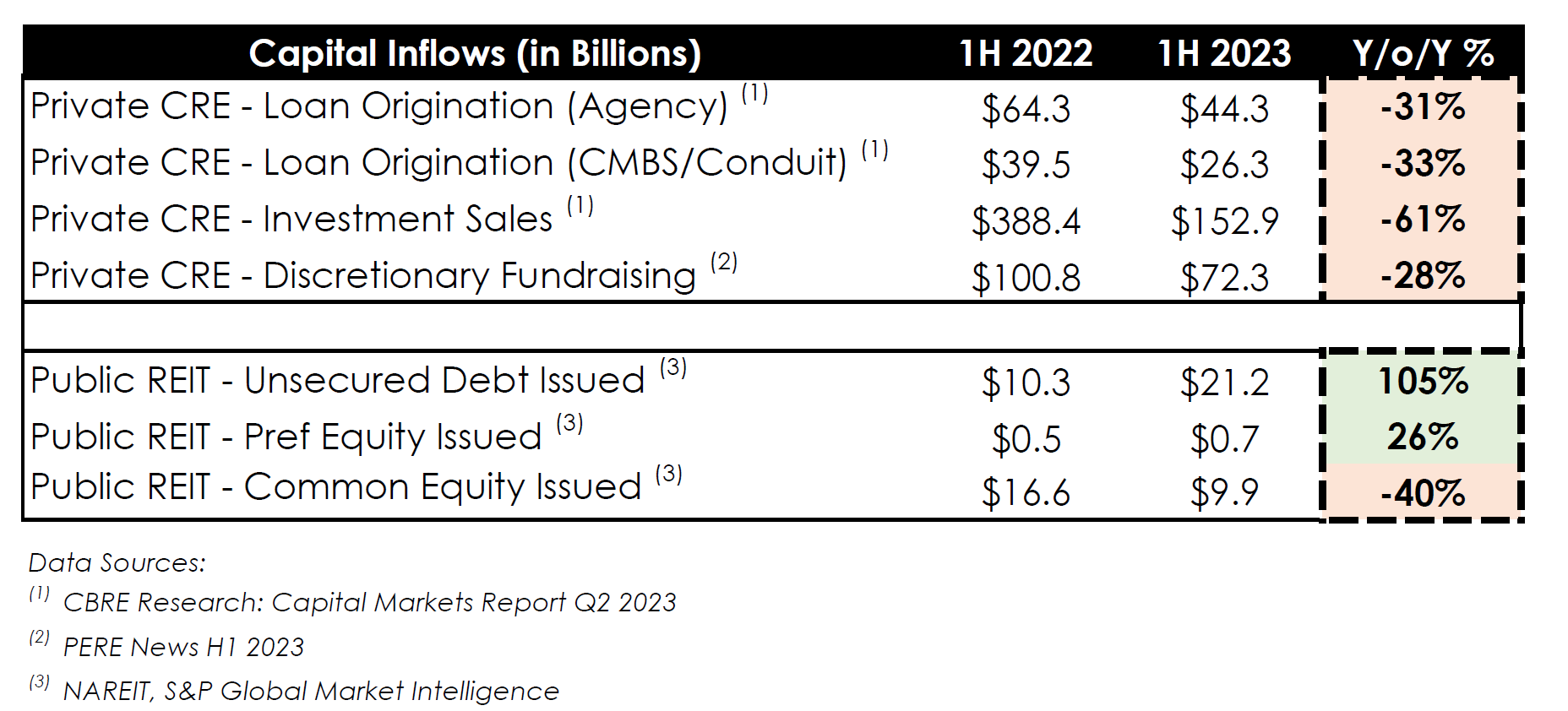

Private commercial real estate (CRE) capital raising was effectively frozen in the first half of 2023. On a year-over-year basis agency financing (Fannie & Freddie) was down -31%, CMBS financing was down -33%, investment sales were down -61% and discretionary fundraising was down -28%.

Meanwhile – except for common equity issuance – capital raising for public REITs has been generally flat-to-up. Unsecured debt issuance was up more than double and preferred equity issuance was up +26%.

On its face it appears public REITs have gone on ‘offense’ by strengthening their balance sheets and raising fresh cash for opportunities, whereas private CRE investors are (seemingly) playing ‘defense’ and remain idle.

There are a few key reasons for the disparity between public REIT activity and private CRE inactivity:

- Public market valuations are considerably cheaper than private market valuations, as implied REIT cap rates are ~200bps higher than private market asking cap rates.

- Public REIT capital is typically more flexible (e.g., unsecured debt, ATM issuance) and buffers unrestricted cash, whereas private CRE capital (e.g. mortgage financing, LP equity) is typically more restrictive between covenants and uses of proceeds.

- Public REITs are typically lower levered (30-50% LTV), whereas private CRE typically utilize max senior leverage (55-70%+ LTV) to turbo-charge returns for LP’s (often private equity funds or private investors seeking higher returns for illiquid allocations).

It is primarily private CRE’s reliance on high leverage financing (#3 above) which has created the perfect storm. With interest rates up >2%+ y/o/y, loan proceeds sizing down, and regional banks (15-20% of the total CRE debt market) out of the picture, the CRE market is (or seems) extremely illiquid.

How can private CRE owners and operators navigate this market – similar to their public REIT peers – to capitalize opportunities?

We are advising our clients to take their heads out of the sand and look downfield. We believe the public REIT approach of proactively raising capital is the right approach for private CRE owners, both in the short term and the long term. There is no one-size-fits-all approach, but below are some the strategies we’re actively discussing with clients. Often we are combining some of these tools if the situation permits.

|

Please reach out to discuss any or all of the above. Most of us were active during the Global-Financial-Crisis (GFC) and – while today’s CRE market is different – the playbook looks very similar: private CRE owners and operators can use this period of short-term dislocation to build long-term value. Public REITs are following the playbook, and so can you. |

About CAMPAIGN Capital

We are the only capital markets firm which focuses exclusively on real estate owners, operators, and developers. We provide a 360° range of advisory services, including project level debt and equity raises, corporate recapitalizations and strategic joint ventures, and consulting and interim CEO/CIO engagements. We draw on our experiences as corporate investment bankers and private equity investors and focus on providing creative and high-touch solutions to our clients. Please reach out to as at info@campaigncap.com to learn more on how we can work together.

{kind=link}